U.S. PE deal value climbed 10.7% year over year in H1 2025, with nearly $1.5 trillion in dry powder waiting to be deployed across equity and debt strategies, according to the 2025 PE Benchmark Report. More capital means more mandates. More mandates mean more stakeholders per deal, more relationships to track, and more data to manage across longer, more complex deal cycles.

Most firms already have a CRM. The problem is that most firms also have a CRM nobody uses.

Generic CRMs built for transactional sales teams force bankers into a workflow that doesn't match how they operate. Investment banking is relationship-driven. When a platform demands manual data entry after every call, every meeting, and every email, adoption erodes. And when adoption erodes, data quality collapses. The CRM becomes a reporting obligation rather than a source of competitive advantage. People update it because they're told to, and the data inside stops being trustworthy.

This is the adoption paradox. CRMs that require manual effort get worse over time, and the less people use them, the less valuable they become… which gives people even less reason to use them.

Tech-forward firms are breaking this cycle. They're adopting platforms that improve with use, automatically capturing communications, enriching records, and surfacing insights without requiring bankers to change how they work. The result is a CRM that compounds in value as more interactions flow through it.

What makes an investment banking CRM different from a general CRM

Most CRMs were built for someone else's job. They assume a linear funnel, a quarterly quota, and a sales rep with time to log everything between calls. Investment banking has none of those things, which is why generic platforms produce the data graveyards firms keep paying for and ignoring.

An investment banking CRM is software purpose-built for deal teams to manage client relationships, track M&A mandates and deal pipelines, and maintain the relationship data that drives mandate origination. It is relationship-driven and deal-centric by design, rather than retrofitted from a sales-funnel template.

Three differences separate investment banking CRMs from general-purpose platforms:

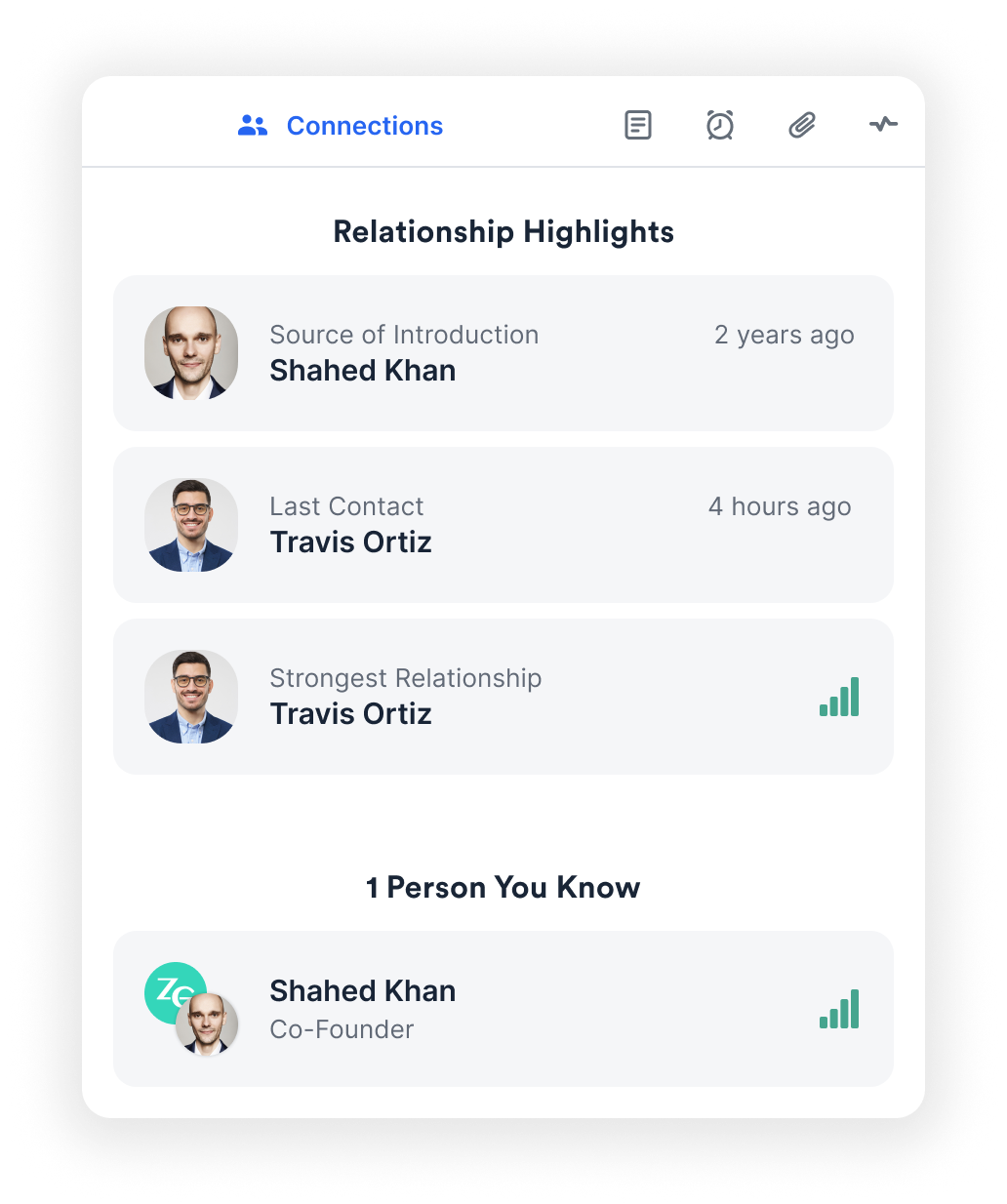

1. Relationship graph vs. contact database. While general CRMs store contacts, investment banking CRMs map who in your firm knows whom at target companies. They surface introduction paths, and quantify relationship strength based on actual interaction history. The difference matters because mandates originate through relationships. A warm introduction to a CEO carries more weight than a cold outreach sequence.

2. Mandate lifecycle vs. linear pipeline. Sales CRMs follow a linear path: lead, opportunity, close. Investment banking deals move through sourcing, execution, and closing, with multiple workstreams running in parallel, shifting stakeholder groups, and timelines measured in months or years. An IB CRM must accommodate this complexity without forcing deals into stages that don't reflect how mandates actually progress.

3. Automatic data capture vs. manual logging. This is where adoption lives or dies. General CRMs require reps to log activities after every interaction. The investment banking CRMs that achieve firmwide adoption capture emails, meetings, and calendar activity automatically. The data enters the system as a byproduct of working.

Take Morgan Stanley’s mandate for the Hinge Health IPO. The outcome wasn’t decided by a single pitch, but by a 15-year relationship between a senior banker and the company’s CFO that spanned three different organizations. This is the exact type of multi-threaded history an IB CRM needs to institutionalize—moving beyond simple data storage to actively surfacing the deep connections that actually win business.

Key features to evaluate in an investment banking CRM

Four capabilities decide whether an investment banking CRM earns its keep: relationship intelligence, mandate management, data enrichment, and security. The rest is feature noise. Below is what each one actually does, and what to look for in a platform that delivers on all four.

Relationship intelligence and automatic data capture

A relationship intelligence layer turns every email and meeting your firm sends into a visible, searchable map of who knows whom, and a relationship without a record might as well not exist. The combination of relationship intelligence and automatic data capture solves both halves of that problem at once. Every interaction enters the system without manual effort, and every interaction becomes part of the relationship graph your team can act on.

Relationship intelligence ingests firmwide email and calendar data, enriches records from 40+ sources, and surfaces introduction paths and engagement history across your entire organization, so the firm's collective network becomes a visible, searchable, and actionable asset instead of a set of disconnected inboxes.

Relationship intelligence is the insight into your team's collective professional network, business relationships, and client interactions that helps you find, manage, and close mandates.

Automatic data capture means every contact, meeting, and email is documented without manual entry, saving deal teams 180+ hours per user annually. This means no logging after calls, updating records before pipeline reviews, or reconciling spreadsheets against inboxes.

Automatic capture produces trusted data, trusted data drives higher adoption, higher adoption generates richer network visibility, and richer visibility leads to better deals. Think of it as a flywheel. Affinity drives adoption rates between 96% and 100% at customer firms because bankers don't have to change how they work. The CRM adapts to them.

The practical impact is significant. When a managing director needs to reach the CFO of a target company, relationship intelligence shows who in the firm has the strongest existing connection, when they last communicated, and the best introduction path. That visibility across every relationship in the firm, including ones outside any one banker's contacts, is what turns a CRM into a mandate origination engine.

Deal pipeline and mandate management

Investment banking deals don't follow a predictable cadence. A mandate can stall for weeks during due diligence, accelerate when a competing bid surfaces, or shift direction when a buyer drops out. Your CRM needs to handle this without breaking.

Purpose-built investment banking CRMs let you visualize complex mandate pipelines alongside contacts, with every opportunity at each stage of the mandate lifecycle, from origination through execution to close. Built-in analytics and reporting track pipeline forecasting, banker productivity, and business development KPIs so leadership has a clear picture of where deals stand and where the firm's time is going.

Collaboration features matter here too. Shared notes, automated reminders, and searchable communication records keep deal teams aligned without requiring yet another status meeting. When multiple bankers are working different angles of the same mandate, the CRM should be the single source of truth, instead of a shared drive folder or a chain of forwarded emails.

The right platform structures this around the IB lifecycle: origination, mandate execution, close. Dealflow management that mirrors how your firm actually operates reduces friction and increases the odds that people will use the system consistently.

Data enrichment and integrations

Research is one of the most time-intensive parts of investment banking. Every new target requires firmographic data, funding history, leadership backgrounds, and competitive context. A CRM that enriches records automatically reduces that burden.

Data enrichment via proprietary and partner datasets populates company and contact records with verified information including investment stage, funding amounts, employee growth, and executive backgrounds. This reduces research time and cuts third-party data costs by consolidating what would otherwise require multiple subscriptions.

Integrations determine whether the CRM becomes the hub of your tech stack or an isolated silo. An open API and native connections to email, file management, social platforms, and financial data providers ensure that relationship and deal data flows where it's needed. A Chrome extension and Outlook add-in keep CRM data accessible wherever bankers communicate, since the best CRM in the world is useless if people have to leave their workflow to use it.

Security, compliance, and privacy

A single compliance failure can damage client trust and regulatory standing in a way that no product feature will offset, which is why security capabilities decide whether a CRM is viable for investment banking before any other feature gets evaluated.

Investment banking firms handle high volumes of sensitive financial data, proprietary deal information, and confidential client communications. SOC 2 Type II, CCPA, and GDPR compliance are baseline. Beyond certifications, look for custom privacy settings that filter sensitive "data exhaust" and prevent capture of confidential details that shouldn't live in a CRM. Granular access controls should limit who can view meeting details, access files, or see specific deal information.

For IB specifically, data protection requirements are heightened because of the volume and sensitivity of information flowing through the firm. The CRM you choose should make it straightforward to enforce data governance policies without creating so much friction that people route around the system.

How leading investment banking CRM platforms compare

Five platforms account for nearly every shortlist an investment banking firm builds. They split into three buckets: purpose-built private capital CRMs (Affinity and DealCloud), enterprise platforms that firms customize for IB (Salesforce), and adjacent tools that bankers consider but rarely standardize on (MadeMarket, HubSpot). The table below compares them on the dimensions that decide adoption and ROI.

Affinity CRM

Affinity is the AI-first private capital CRM. It automatically builds a relationship graph from firmwide communications, including every email, meeting, and calendar interaction, and enriches that data from 40+ sources to create a living picture of your firm's network.

The numbers back the approach: 3,300+ private capital firms trust Affinity, including 40% of the global VC market by firm count. The platform's relationship graph contains 500M+ structured relationships built from 22B+ captured emails and calendar events. Firms typically see their network become visible and actionable within 24 hours of setup, instead of after a months-long implementation project.

Customers like Munich Re Ventures report 96% firmwide monthly adoption, and firms like BDev Ventures and FoW Partners hit 100%, because the platform captures data automatically and delivers value without requiring bankers to change how they work. Deal teams save 180+ hours per person annually, time that goes back into origination and client relationships instead of CRM maintenance.

"Our clients want to know that we have key access to decision-makers. We’re able to show them this by showing them the core of our CRM system—Affinity. It’s about being honest and truthful—that is what matters to clients.” — Mirko Heide, Managing Director at IEG

DealCloud by Intapp

DealCloud positions itself as all-inclusive financial services software spanning marketing, pipeline management, fundraising, and business development. It offers deep customization and end-to-end deal lifecycle management, particularly for large firms with complex workflows that span multiple business lines.

The trade-off is implementation. DealCloud deployments are time-consuming and typically require dedicated consultants, with timelines often measured in months. For firms that need extensive customization and have the resources to support a lengthy implementation, DealCloud can be a fit. For firms that want to move faster, the timeline and cost may be prohibitive.

Learn more about DealCloud and how it compares to Affinity

Salesforce

Salesforce is the most widely deployed CRM in the world, and a meaningful share of bulge bracket and large investment banks run on it. This is often because the firm standardized on Salesforce across business lines years before the IB team had a dedicated say in the decision. With enough configuration, Salesforce can model mandate pipelines, track coverage relationships, and integrate with the financial data providers IB teams rely on.

The trade-off is the configuration itself. Salesforce was built for transactional B2B sales motions, not multi-year mandate cycles, so adapting it to investment banking typically requires custom objects, custom workflows, third-party app marketplace components, and three to six months of implementation work with dedicated consultants. Relationship intelligence isn't native, so firms layer it in through add-ons. Automatic activity capture isn't native either, which means adoption often hinges on whether bankers actually log their activity, which is the same adoption problem that drives firms to evaluate purpose-built platforms in the first place.

For firms already committed to Salesforce across the enterprise, the platform's flexibility, ecosystem, and security posture (SOC 2, ISO 27001, GDPR) make it a defensible choice. For firms starting fresh or evaluating IB-specific options, the configuration overhead and missing relationship layer are real considerations.

MadeMarket

Founded by former finance professionals, MadeMarket offers a lightweight, IB-specific CRM with workflow management and customization for business development and deal execution. It's designed for small teams that want a focused tool without the complexity of enterprise platforms.

The limitations are real. MadeMarket relies on manual data management with no automatic capture, which means adoption depends entirely on discipline. MadeMarket holds SOC 2 Type I and Type II certification, but its broader compliance coverage is narrower than enterprise-grade platforms, which may matter for firms with international operations or strict institutional LP requirements.

HubSpot

HubSpot is strong for marketing automation and website hosting, and its free basic CRM is an accessible starting point for firms with limited budgets. The platform excels at inbound marketing workflows and content management.

However, investment banking teams will find many HubSpot features irrelevant, and its inbound-marketing orientation limits its usefulness for relationship-driven mandates. HubSpot is built around attracting and converting leads through content, a model that doesn't map to how IB firms originate deals through relationships, introductions, and network leverage.

CRM evaluation checklist for investment banking teams

The wrong CRM costs more than the subscription. It costs the time bankers spend working around it, the deals that slip when data is stale, and the months of consultant fees that follow a complex implementation. Use this tiered checklist to prioritize what actually matters in your evaluation:

Tier 1, must-have:

- Relationship intelligence. Surfaces introduction paths and firmwide network visibility.

- Automatic data capture. Logs emails, meetings, and contacts without manual entry.

- Mandate pipeline management. Tracks opportunities through sourcing, execution, and closing.

- Enterprise-grade security. SOC 2 Type II, GDPR, and CCPA compliance at minimum.

- Mobile access. Pipeline, contacts, and relationship intelligence available on the go through a purpose-built mobile app.

Tier 2, important:

- Data enrichment. Proprietary and partner datasets reduce research time.

- Open API and integrations. Connects to email, data providers, and file management tools.

- Built-in analytics. Pipeline forecasting, banker productivity, and BD reporting.

Tier 3, nice-to-have:

- Cross-functional tools. Integration with marketing, customer success, or traditional sales teams.

- Enterprise-wide scalability. CRM that grows with firm size and deal complexity.

- Additional non-CRM products. Broader software suite for connected workflows.

{{a4s-request-demo-b="/rt-components"}}

Frequently asked questions

What is the best CRM for investment banking?

The best investment banking CRM depends on firm size, deal volume, and workflow requirements. Affinity is the AI-first private capital CRM, with automatic activity capture and Relationship Intelligence that drive firmwide adoption. It is particularly effective for middle-market and boutique banks. Salesforce offers deep customization but requires significant implementation. DealCloud provides end-to-end deal lifecycle management.

What features should an investment banking CRM have?

An investment banking CRM needs deal pipeline management, automatic activity capture, relationship intelligence, pipeline analytics, and enterprise-grade security (SOC 2, GDPR). The most important distinction is between CRMs that require manual logging and those that capture activity automatically. Automatic capture drives dramatically higher adoption.

What is CRM in investment banking?

CRM in investment banking is software that helps deal teams manage client relationships, track M&A mandates and deal pipelines, and maintain the relationship data that drives mandate origination. Unlike sales-focused CRMs, investment banking CRMs handle complex, multi-stakeholder deal lifecycles where relationships generate business.

Do investment bankers use special CRMs?

Yes. Most IB teams find general-purpose CRMs don't fit relationship-driven, deal-centric workflows. Common approaches include adopting Affinity, which automatically captures communications and maps firmwide networks for middle-market and boutique banks; configuring Salesforce with IB customizations for bulge bracket banks; or using DealCloud for end-to-end deal management at large PE-adjacent firms.

How much does investment banking CRM software cost?

Enterprise platforms like Salesforce run $150 to $300+ per user/month with implementation costs often exceeding the subscription. Purpose-built IB CRMs typically range $50 to $150 per user/month with faster implementation. Total cost of ownership should include implementation time, training, and ongoing adoption support.

How does a CRM help investment bankers manage deals and client relationships?

A CRM centralizes deal and relationship data in one platform, replacing scattered spreadsheets and email threads. It tracks every interaction across the firm's network, manages mandate pipelines from origination through closing, and surfaces introduction paths to decision-makers. Affinity goes further by automatically building and maintaining this data without manual entry.

What are the differences between general CRMs and investment banking CRMs?

General CRMs are built around linear sales funnels (lead, opportunity, close), while investment banking CRMs support complex mandate lifecycles with multiple stakeholders. IB CRMs prioritize relationship mapping over contact management, capture deal-specific data (mandate types, transaction stages, buyer lists), and integrate with financial data providers rather than marketing tools.

How long does it take to deploy an investment banking CRM?

Deployment varies significantly by platform. Salesforce with IB customizations can take three to six months with dedicated consultants. DealCloud implementations are similarly extended. Affinity deploys firmwide in under 60 days without consultants, and firms typically see their network become visible and actionable within 24 hours of setup.

Ready to see what relationship intelligence looks like for your firm?

Talk to sales for teams ready to evaluate Affinity CRM.