Unicorns abound in Europe. Will global economic turmoil thin the herd?

In 2019 Matt Miller—a partner with Sequoia Capital—predicted a far-fetched event: the birth of a bumper crop of unicorns, thanks, in part, to a technology boom on in Europe.

Today, the number of unicorns in Europe is on a steep upward climb. Europe produced 5x more unicorns in 2021 than in 2020. And it’s producing tech unicorns at more than 2x the rate of the U.S.

At the end of 2021, Europe was home to over 390 unicorns—private startup companies valued at over $1 billion. 1/3 of those passed the billion dollar mark in 2021 alone. European unicorns are now worth a combined $1.6 trillion, up 305% in the last 5 years. And half that value is linked to decacorns: a private company valued at $10+ billion.

Today, thanks in part to Miller’s prescience, Sequoia owns stakes in 1/5 of all European unicorns.

Pessimists, optimists, and unicorns

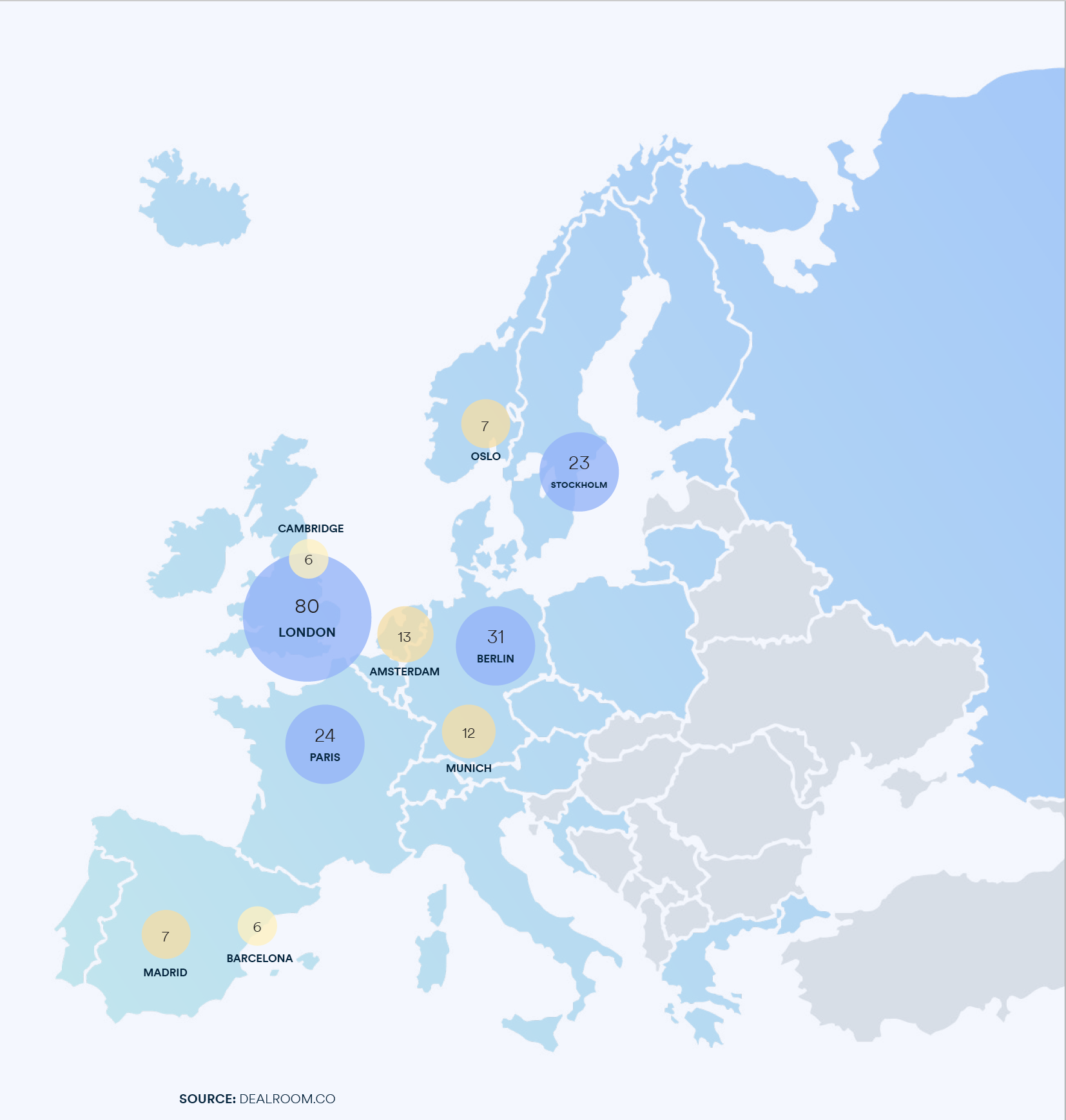

A decade of growth for European venture capital investments—spurred in part by cash from the other side of the Pond—has led to the steady increase in these billion-dollar beasts. The UK, freed by Brexit of complex European Union regulations, is home to more billion-dollar companies than any other European country: 1/3 of all European unicorns.

24 European countries have produced more than one unicorn, and Europe is home to 65 “unicorn cities.”

Few expect 2022 to match the skyrocketing activity of 2021. That activity resulted from the large stores of dry powder VC’s accumulated during 2020’s pandemic-related lockdowns. The dropoff in business activity during the first half of 2022—catalyzed by the war in Ukraine, frightening inflation, and global recession fears—could foreshadow a similar dropoff in everything from fundraising to unicorn creation.

While private equity dealmaking worldwide has proved resilient so far, European exits have declined. And at the end of Q2, fundraising levels were only 25% of 2021’s total.

Ongoing concern is how centralized investment sources have been. A single VC, London-based Index Ventures, had its hand in 10 of the continent’s largest decacorns. Down-rounds and layoffs are on the rise, the timelines for payouts to limited partners are lengthening, and there has been some decrease in valuations. That in itself will cull the unicorn herd as portco values fall below $1 billion. Tranched financings and other risk-reduction funder tactics are becoming more common. Some are even doling out advice to put up “for sale” signs.

VC business volume in 2022 is dipping. But the worldwide economic downturn that began this year is not reflected in all industry benchmarks, startup fundraising, or investment activity.

“The best companies will keep their foot on the gas. It doesn’t take as much strength when it’s easy to fundraise. But the playing field is getting tougher, which will benefit people who can make the most of the opportunity,” noted Michelle Bailha, a partner and colleague of Miller’s at Sequoia.

European unicorns, American money

That optimism is not unfounded. The total value of decacorns in 2021 was $777.4B; in June of 2022, it was already $730.4B, putting it on track to exceed 2021’s number. While the UK outperforms the rest of Europe in unicorn volume, Germany, France, Scandinavia, and Benelux are adding unicorns at a healthy rate as well.

“The geographic map of opportunity is only getting larger and more complex,” observed Miller more recently. At least 7 industries—led by fintech and health—comprise at least 5% of European unicorn-based value. That will spread risk across industries likely to be affected differently by the economic volatility currently wreaking havoc at tech startups.

U.S.-based VCs like Sequoia have opened offices across Europe and are contributing larger percentages of the funding to European startups—a full 35% in 2021. This, too, will spread risk: across unicorn-generated wealth across the U.S., UK, and the entirety of the European Union’s economies.

Putting dollars that might have gone to U.S. companies into Europe also signaled confidence in the European startup market. Whatever the original source of American VC’s attraction to the European market had been, this diversification could make for a softer landing for LPs and VCs at the end of a bumpy ride. And it may even accelerate the ascendence of the European unicorn.

For more information on the state of the European unicorn economy, including charts and graphs with the specifics of the data referred to in this post, click the image below to access Affinity’s recently released Relationship Intelligence Benchmark Report: European Unicorn Edition.

Related Articles

Put your firm’s network to work