The venture capital benchmark report: 2025 edition

Is your firm keeping up with top VCs?

Our annual venture capital benchmark report analyzes exclusive data from almost 3,000 VC firms across 68 countries—providing the insights you need to stay competitive.

Explore key benchmarks on deal volume, network activity, and engagement data to learn:

- How dealmaking activity trends have shifted over the past 12 months

- What top performing firms do differently

- Ways to strengthen your deal sourcing and portfolio support strategies

"Implementation was really easy. We were able to start using the platform straight away."

"Having a well-defined, clean, golden source data set is more important in the age of AI. That's a lot of the benefit we're seeing from Affinity."

"It's night and day. We are way more organized when it comes to relationships. We've won a good amount of deals we wouldn't have won if we hadn't changed over to Affinity."

"Venture capital is a craft, and Affinity is one of the tools helping the investment team build this craft better."

The venture capital benchmark report: 2025 edition

.webp)

Why read this report?

01. Market trends

Understand how VC dealmaking activities have evolved over the past year and present challenges.

02. Benchmarks of top firms

Learn what differentiates top VC firms and see how your firm’s activities compare.

03. Practical guidance

Get actionable insights into adapting your deal strategies to get ahead this year.

INTRODUCTION

A year of highs and lows for venture capital

2024 was a year of contrasts for private markets. On the one hand, global venture capital (VC) deal activity showed growth, particularly in the U.S., which saw a 29% year-over-year (YoY) increase in deal value.

At the same time, activity became increasingly concentrated by size, sector, and players. The number of mega deals surged—especially in AI and machine learning, which accounted for 36% of global VC deal value—while the number of first-time funds fell to a decade low.

In this context, we analyzed Affinity data on almost 3,000 VC firms across 68 countries (who we refer to as “All Firms”) versus a subset of those ranked as top investors by Dealroom’s VC Investor Ranking (who we refer to as “Top Firms”). The data analyzed includes email volume, introductions made, and the number of deals and new contacts added to Affinity, offering valuable insights into key VC dealmaking practices.

Keep reading to uncover three key challenges and opportunities the industry faces and the dealmaking activities that differentiate Top Firms.

29% year-over-year (YoY) increase in deal value in the U.S.

CHAPTER 01

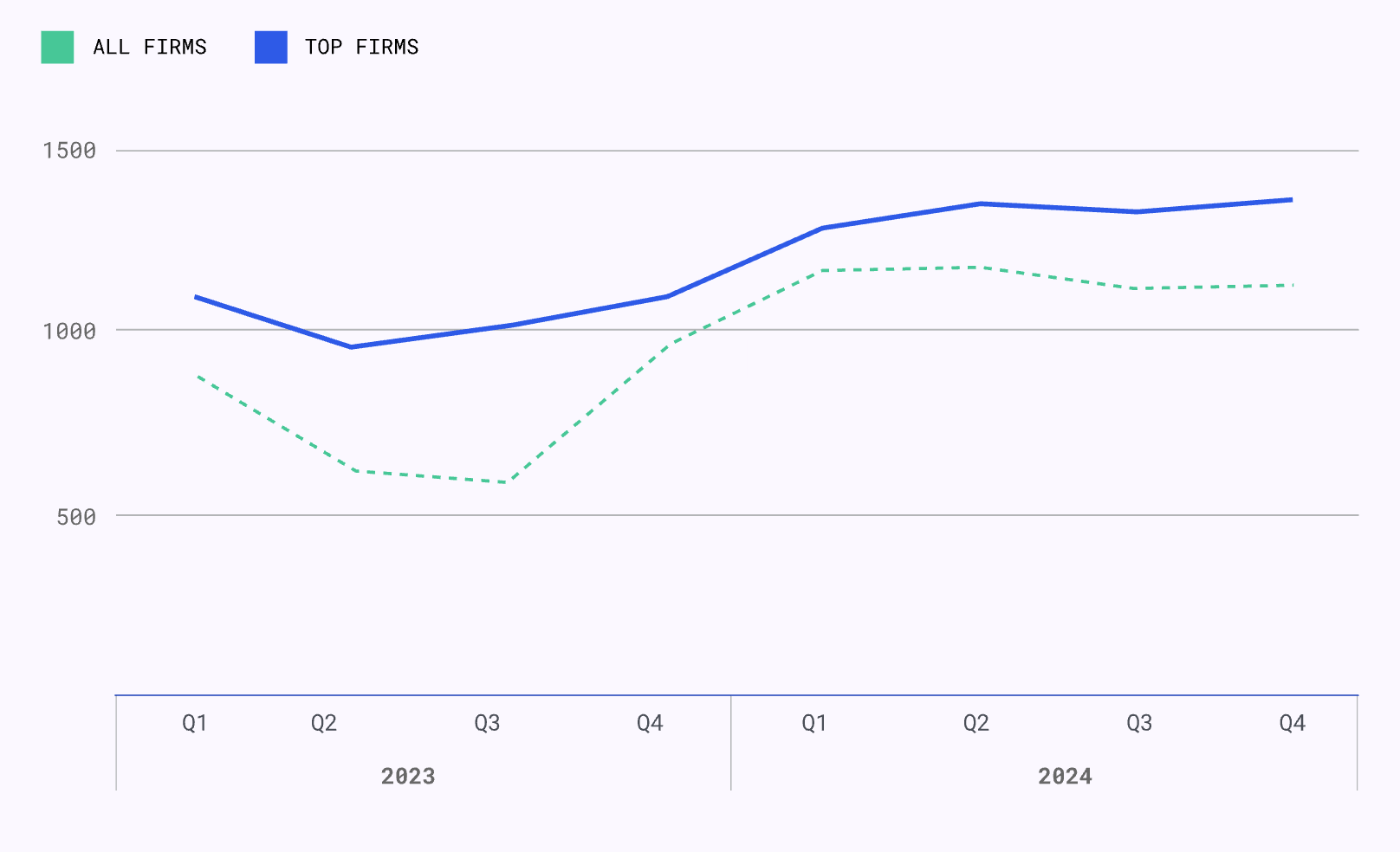

Competition for deals is tight

source: AFFINITY

Top Firms continued to hold the lion’s share of deals in 2024, working on more than twice the number of deals as All Firms throughout the year. However, their deal flow was volatile and significantly lower than in 2023—suggesting Top Firms weren’t immune to tougher dealmaking conditions.

What’s driving this? Top Firms appear to be more selective—prioritizing stricter diligence and companies with more promising growth potential—but also ready to act when opportunities arise. Many are likely focusing on fewer but larger deals. In 2024, average VC deal size increased across all stages, contributing to a 5% YoY increase in global VC deal value—despite a decline in deal count.

Meanwhile, All Firms saw a steady decline in deal flow, ending 2024 with 17% fewer deals YoY. All Firms appear to be feeling the heat of competition, which 42% of investors cite as the biggest factor impacting deal flow—leaving many firms unable to secure deals even when activity picks up.

CHAPTER 02

Outbound deal sourcing is gaining traction

source: AFFINITY

Engagement rose—and was more consistent—in 2024 for All Firms, who sent and received 17% more emails YoY in Q4. After two slow years of dealmaking, All Firms likely ramped up outreach efforts to source new deals, which is the top priority for 50% of investors.

Top Firms also saw increased engagement, though primarily for a different purpose (more on that in chapter 3).

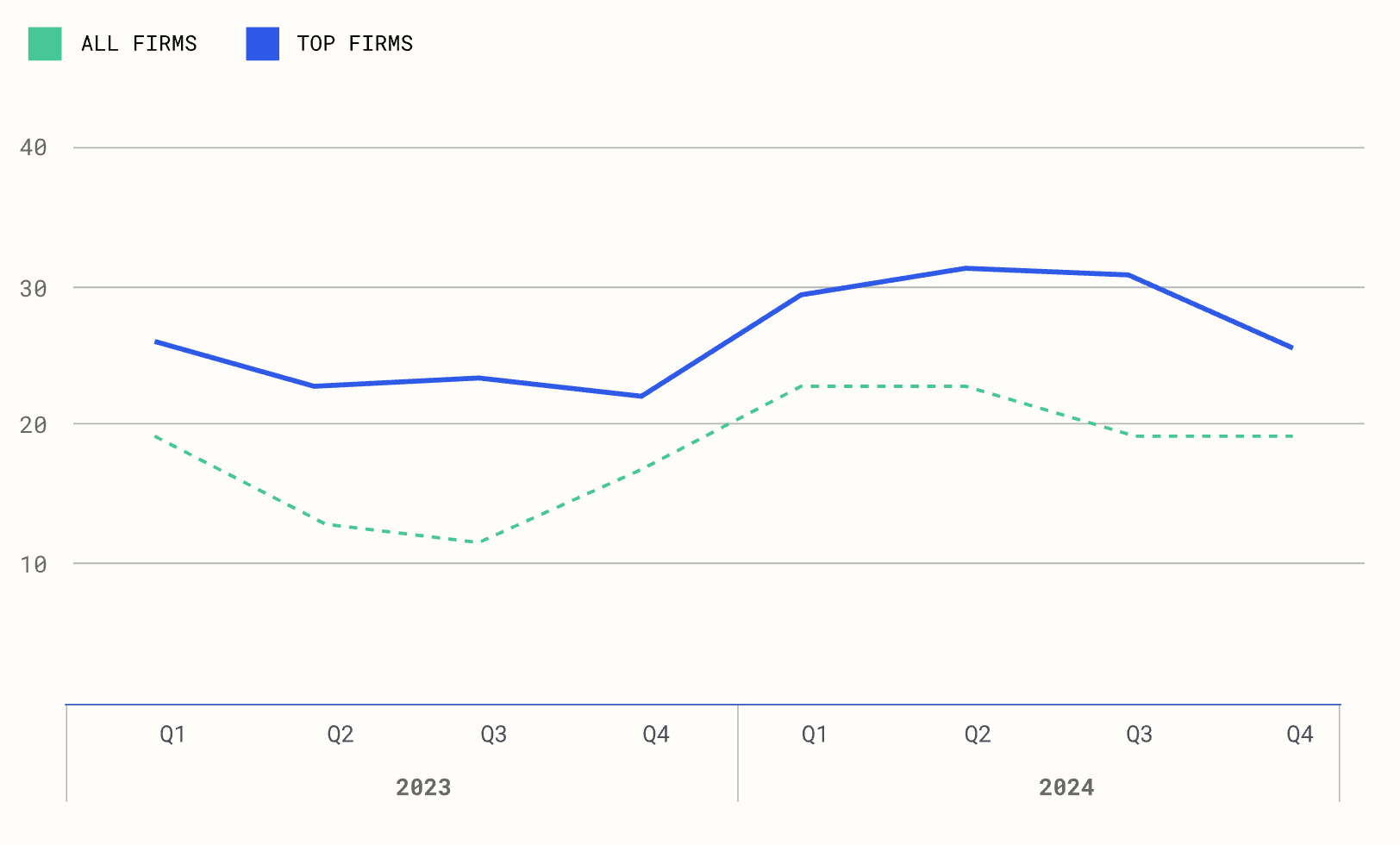

Median number of contacts added per user

source: AFFINITY

All Firms outpaced Top Firms in network growth in 2024, particularly in Q1 when they added 11% more contacts. Despite slower network growth for the rest of the year, All Firms ended 2024 with a 4% YoY increase in new contacts—suggesting they ramped up outreach at the start of the year before shifting to a more targeted approach.

As competition intensifies, more firms are moving from inbound deal sourcing to outbound strategies powered by data-driven insights and technology.

CHAPTER 03

Portfolio support takes center stage

Median number of contacts added per user

source: AFFINITY

Looking more closely at the median number of contacts added per user, Top Firms saw two consecutive quarters of network growth in 2024, but ended the year with 4% fewer new contacts YoY. This indicates that they shifted toward prioritizing existing relationships for deal sourcing and portfolio support, since engagement increased while network growth fell.

Median number of introductions made per user

source: AFFINITY

Top Firms consistently made more introductions than All Firms throughout 2024, ending the year with a 16% YoY increase. As deal flow slowed in Q2 2024, Top Firms likely shifted to supporting their portfolio companies midyear—connecting them to talent or potential customers—since introductions rose while network growth declined.

While liquidity remains challenged, the pressure is on to deliver returns and reinforce LP confidence—especially for firms planning to fundraise in the near future. In response, Top Firms are hyperfocused on maximizing portfolio growth to demonstrate the ongoing value of their funds and ensure each company achieves a positive exit, whenever that may be.

CHAPTER 04

Strategies of Top Firms

The trends in this report reveal three key differences in the dealmaking activities of Top Firms:

1. Increased selectivity

While Top Firms saw a decrease in deal volume in 2024, this reflects a deliberate shift toward greater selectivity—prioritizing quality (and size) over quantity of investments.

These firms are focusing more on finding, screening, and selecting companies with the most promising growth potential—using data and technology to track deal signals, streamline research, and identify the right opportunities as early as possible. The biggest VCs are investing heavily in data-driven sourcing, and more than half (64%) of investors now use AI to accelerate company research.

2. Consistency in engagement

Similarly, Top Firms are favoring quality over quantity with their network, nurturing existing connections through emails and regular check-ins

With 42% of investors citing competition as the biggest factor impacting deal flow, maintaining sustained engagement (especially in tougher markets) helps firms stay top of mind with prospective founders, reduces uncertainty for LPs, and enables them to capitalize on overlooked opportunities when deal flow picks up.

3. More effective use of their network

When deal flow slowed midyear, Top Firms doubled down on portfolio support—increasing engagement and making more introductions on behalf of their portfolio companies.

By connecting founders with industry experts, vendors, and potential customers, these firms use their extensive networks to help drive growth and provide value beyond capital.

64% of investors use AI to accelerate company research.

42% of investors say competition is the biggest factor impacting deal flow in 2025.

source: Affinity’s 2025 private capital predictions report

CHAPTER 05

Navigating a more competitive dealmaking landscape

On the whole, 2024 was a year marked by intense concentration and large events propping up an otherwise sluggish venture market. Just 20 VCs captured 60% of the total capital raised, making it increasingly difficult for smaller, less established firms to get in on deals before their competition.

Despite these challenges, many investors remain optimistic about 2025; more than 70% of dealmakers expect to close more deals compared to last year.

For firms to succeed in this competitive environment, it will be crucial to balance a strategic, data-driven approach to deal sourcing with the fundamentals of venture capital: relationship building. Success hinges on strengthening existing relationships through consistent communication across the entire VC ecosystem, engaging with founders, LPs, co-investors, and strategic advisors to stay agile and capitalize on opportunities as they arise.

“All of us are trying to achieve the same thing: find companies early, invest in them, grow them, and get great exits… Invest in scalable solutions. Invest in your data. It's not always about the tools you're using, but about your ability to aggregate your data.”

Moustafa ElBialy

CIO at Kleiner Perkins

Elevate your dealmaking with Affinity

Affinity combines AI, deal data, and relationship insights to streamline your entire dealmaking process—from sourcing to portfolio support and fundraising.

With Affinity, you can:

- Find the right deals: Discover and track high-potential opportunities using data enrichment, growth signals, and opportunity watchlists. Join the waitlist for Affinity Sourcing.

- Win deals before your competitors: Accelerate outbound deal sourcing by understanding the strength of each relationship in your firm’s network and the strongest introduction path, and fast-track company research with Industry Insights, Affinity’s AI-driven market intelligence tool.

- Fuel portfolio growth: Effectively respond to founder requests, share timely updates with investors, and demonstrate your firm’s value to founders and LPs with centralized tracking and comprehensive analytics.

About our data

The Affinity platform data displayed in this report is aggregated and anonymized. It represents the dealmaking trends of more than 2,800 VC firms (“All Firms”) versus a subset of those ranked as top investors by Dealroom’s VC Investor Ranking who use Affinity (“Top Firms”).

Dealroom defines top investors in their Global Combined Ranking as: “A ranking of venture capital investors, based anywhere, investing in companies anywhere, and at any stage. The ranking looks at how successful investors are at picking startups that go on to big outcomes – primarily looking at unicorns and future unicorns (companies valued $250M-$1B). Investments are weighted by the stage at which firms invest in the most successful companies, with the aim of creating insights from a level playing field, e.g. most points for backing a unicorn at Seed, then Series A and so on.”

The data in this report uses median figures to provide an accurate picture of how the market has evolved on a quarterly basis from 2023 - 2024.

The information in this report is provided for general informational purposes only. While efforts have been made to ensure its accuracy, no warranties or representations are made regarding the completeness or reliability of the content. Project Affinity, Inc. is not liable for any losses or damages arising from the use of this report. This report does not constitute professional advice. For specific concerns, consult a qualified expert.

.webp)

.webp)

.webp)