Private capital predictions for 2026

Private capital enters 2026 at an inflection point—and the winners are already separating from the pack. After years of uncertainty, investors are finding their footing with renewed optimism tempered by strategic discipline.

Our survey of nearly 300 private capital professionals shows how firms are adapting as the fundraising landscape shifts and pressure to prove value intensifies. From AI adoption to data consolidation, firms are fundamentally rethinking how they source, evaluate, and close deals.

Read the report to uncover:

- Why data consolidation is accelerating as AI adoption surges

- How firms are sustaining their focus on deal sourcing efficiency

- Why the fundraising window is opening—and why proving value now matters more than ever

"Implementation was really easy. We were able to start using the platform straight away."

"Having a well-defined, clean, golden source data set is more important in the age of AI. That's a lot of the benefit we're seeing from Affinity."

"It's night and day. We are way more organized when it comes to relationships. We've won a good amount of deals we wouldn't have won if we hadn't changed over to Affinity."

"Venture capital is a craft, and Affinity is one of the tools helping the investment team build this craft better."

Private capital predictions for 2026

.webp)

Private capital enters 2026 at an inflection point—and the winners are already separating from the pack.

After years of economic uncertainty and market turbulence, investors are finding their footing with a renewed sense of optimism tempered by strategic discipline.

The fundraising landscape has transformed dramatically. Yet this optimism exists alongside intensifying pressure to demonstrate value in an increasingly competitive environment.

Our latest survey of nearly 300 private capital professionals reveals how the industry is adapting to this evolving reality. From technology and tooling to data consolidation strategies, firms are fundamentally rethinking their approach to dealmaking.

Three forces will define who wins in 2026:

- Data consolidation accelerates as AI adoption surges

- Firms will sustain their focus on deal sourcing efficiency

- The fundraising window will open, but proving value will define success

Research shows that more than half of dealmakers see improved fundraising prospects compared to the previous year, while Adams Street pairs these prospects with competitive pressures and a need for disciplined execution. Limited Partner (LP) demand is strong but selective, favoring resilient and flexible General Partners (GPs). There is anticipation of a continued fundraising uptick in early 2026 despite ongoing challenges.

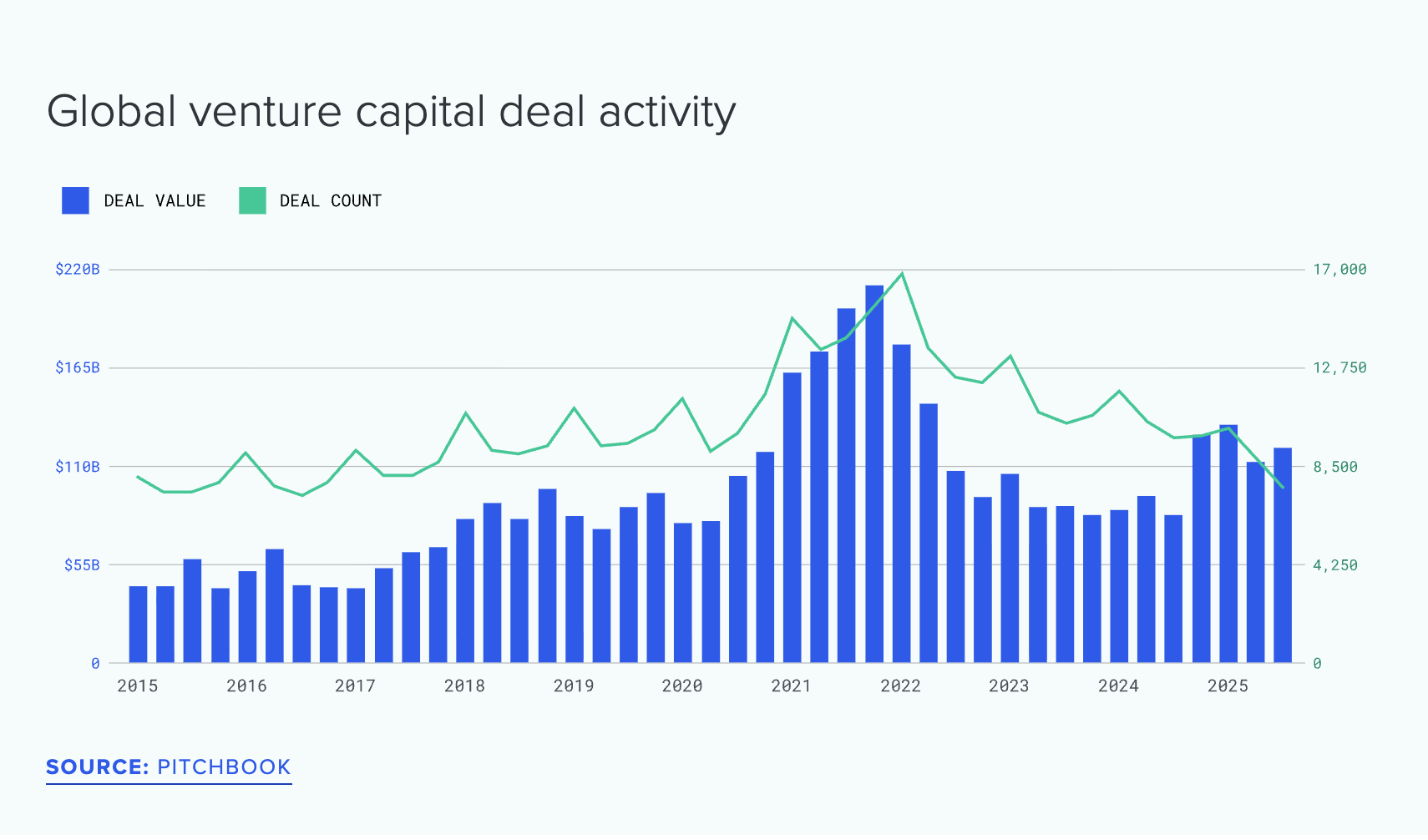

Meanwhile, Bain reports that generative AI funding grew at an accelerated pace last year, with the first half of 2025 raising more than all of 2024 combined. Software and AI companies now command roughly 45% of all venture capital investments. The firms that adapt now will dominate.

Keep reading to learn what investors predict for 2026 and how leading firms are preparing now.

Our predictions

01. AI will evolve from experimentation to strategic expansion

02. Firms will sustain their focus on deal sourcing efficiency

03. The fundraising window will open, but proving value will define success

PREDICTION 01

AI will evolve from experimentation to strategic expansion

The 2026 data reveals a fundamental shift in how private capital firms approach artificial intelligence. After years of cautious experimentation, AI adoption has surged across all use cases—with one particularly dramatic change signaling a new era of confidence in AI-assisted decision-making.

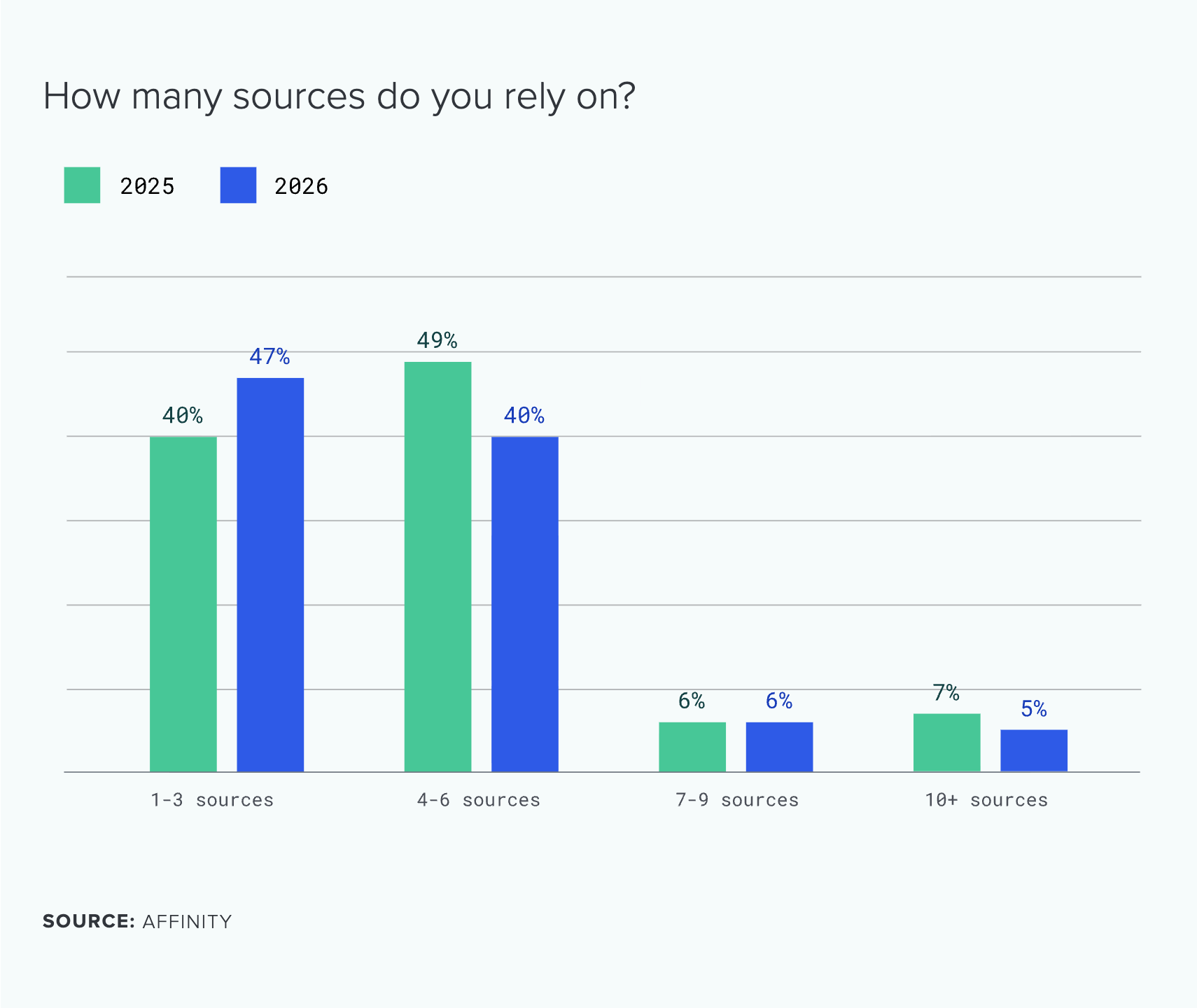

Data consolidation accelerates dramatically

One striking change in 2026 is the rapid consolidation of data sources. Firms are moving decisively away from sprawling technology stacks toward more focused, high-value solutions:

The "sweet spot" appears to be shifting from 4-6 sources to 1-3 sources, suggesting firms have moved beyond experimentation and are focusing on core, integrated data platforms that deliver genuine value.

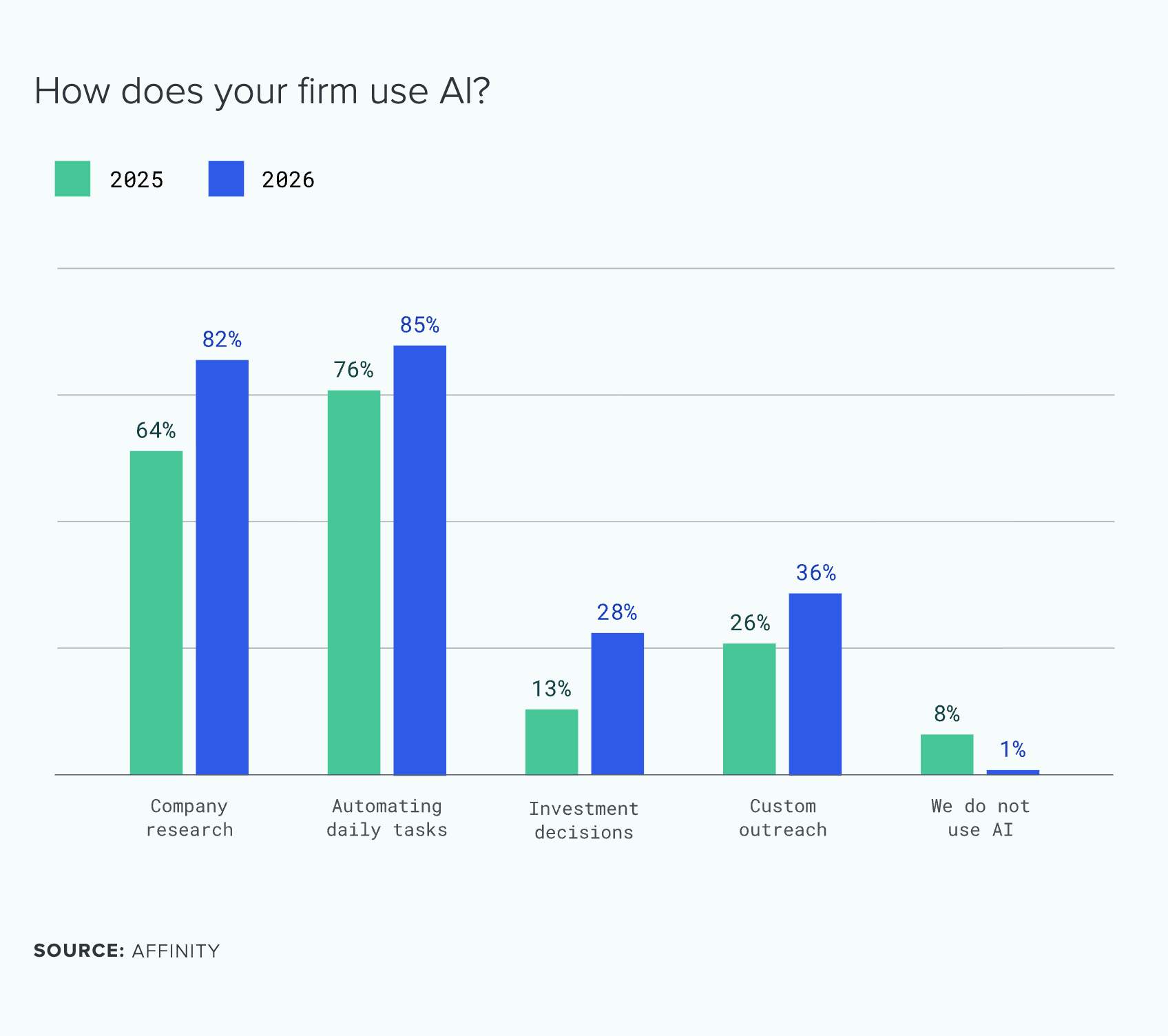

AI usage soars across all categories

Compared to 2025, AI adoption has accelerated significantly:

The most striking change is in AI for investment decisions. This metric more than doubled.

This transformation suggests firms have found more effective ways to integrate AI into decision-making workflows without replacing human judgment. The technology has matured from a curiosity to a strategic tool that enhances rather than supplants investor expertise.

Brian James Murphy, Lead Data Scientist at Salesforce Ventures, reinforces this perspective: "I really want to make sure our team has the right information at the right time, and it doesn't necessarily replace their judgment or try to mimic their judgment, it's just augmenting it."

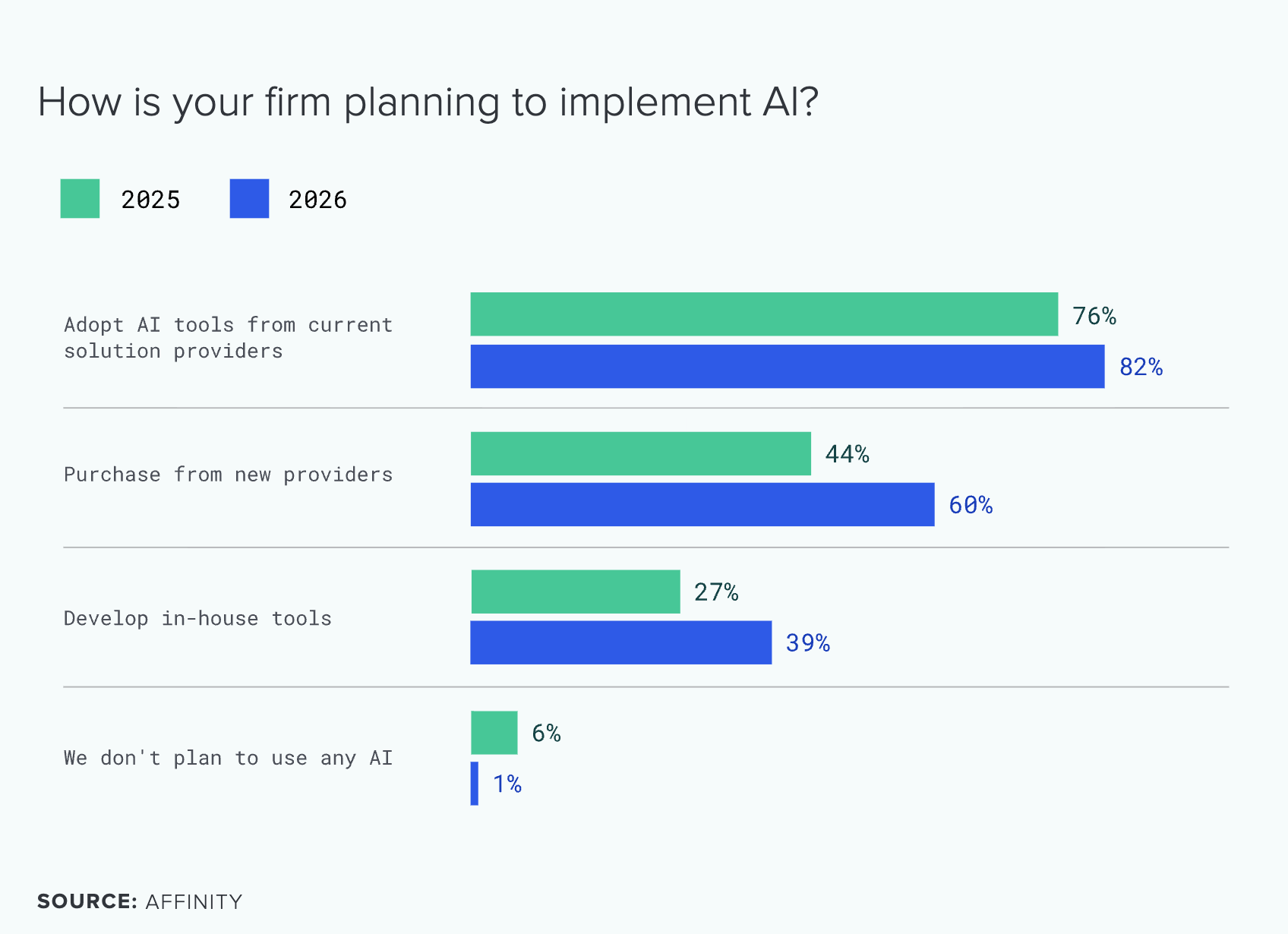

Firms pursue multi-channel AI strategies

When it comes to implementation, firms are taking a diversified approach:

This pattern indicates that AI adoption is no longer an either/or decision. Leading firms recognize that effective AI integration requires a combination of vendor solutions and custom development tailored to their specific workflows.

“This year, there's been a real shift in AI's capabilities," said David Hefter, AI Champion for Investments at Blackrock. "With reasoning models came tool calling, web search, and additional capabilities built on top of that. It unlocked an ability to get so much more value out of using AI tools."

The equilibrium that wasn't

In 2025, we predicted that data and AI complexities would reach an equilibrium as firms settled into stable technology stacks. The 2026 data tells a different story.

Rather than plateauing, AI continues to expand its role across private capital operations. The dramatic jump in AI for investment decisions suggests we're still in the early innings of this transformation.

Mercedes Bent, Venture Partner at Lightspeed, highlights the productivity gains: "It used to take me three or four days to write a memo. Now, with the help of AI and deep research, I can get it done in four to six hours."

The consolidation we see in data sources coexists with expanding AI capabilities—firms are simplifying their data infrastructure while simultaneously deepening their AI integration. This isn't equilibrium; it's strategic evolution.

"In 2026, I foresee: Continuation funds and secondary share sales will continue to mature as legitimate exit options — especially for long-dated investments wanting liquidity without full exit. Investors will demand more rigour, possibly forcing down rounds or impairments for weaker assets. Extended holding periods will become more common where market timing is unfavorable. GPs will continue to face pressure to deliver liquidity to LPs, though some will succeed via creative structuring."

Itamar Eliash

Investment Team, Symbol

From tool to teammate

The most significant shift in AI adoption isn't about the percentage of firms using it; it's about how they're using it. The leap in AI for investment decisions signals a fundamental change in investor confidence. AI has moved from the periphery of operations (automating notes, summarizing research) to the core of decision support.

Yet let’s be clear: AI augments rather than replaces judgment. Firms that are seeing the greatest returns from AI aren't those replacing human decision-making. They're those who've found the optimal balance between algorithmic insight and investor nuance and intuition.

This maturation creates a new competitive dynamic. Success in 2026 won't come from simply having AI tools. It will come from integrating them seamlessly into workflows where technology handles pattern recognition and data synthesis, freeing investors to focus on relationship building and strategic thinking.

PREDICTION 02

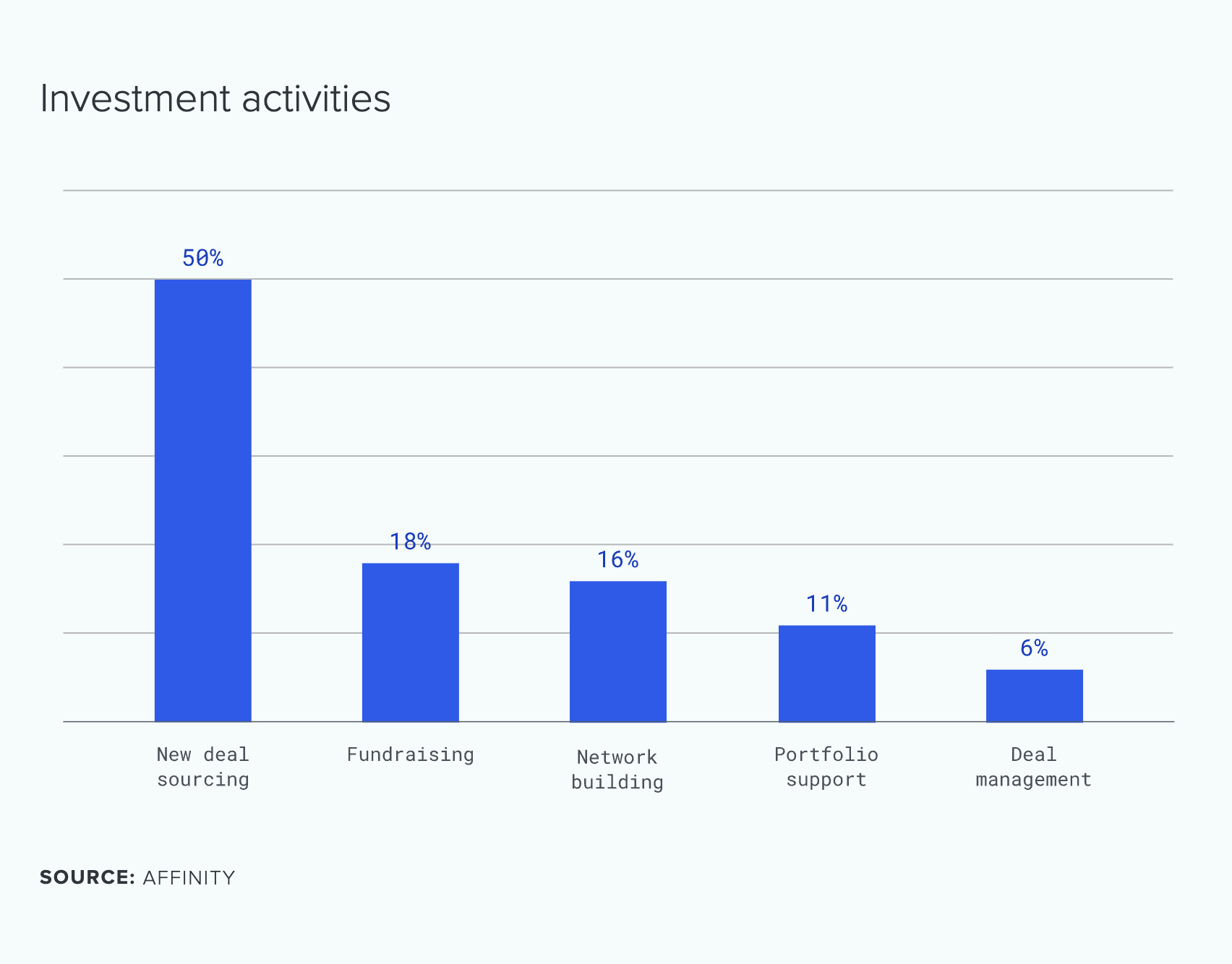

Firms will sustain their focus on deal sourcing efficiency

Deal sourcing maintains its position as a critical priority for private capital investors in 2026, with half of respondents ranking it as their primary focus. While this represents a slight moderation from 2025's peak, the numbers tell a story of maturation rather than retreat.

50% of investors ranked new deal sourcing as their top priority in 2026, which is flat year-on-year. This suggests a steady trend compared to 2024 when new deal sourcing was a top priority for only 30% of dealmakers.

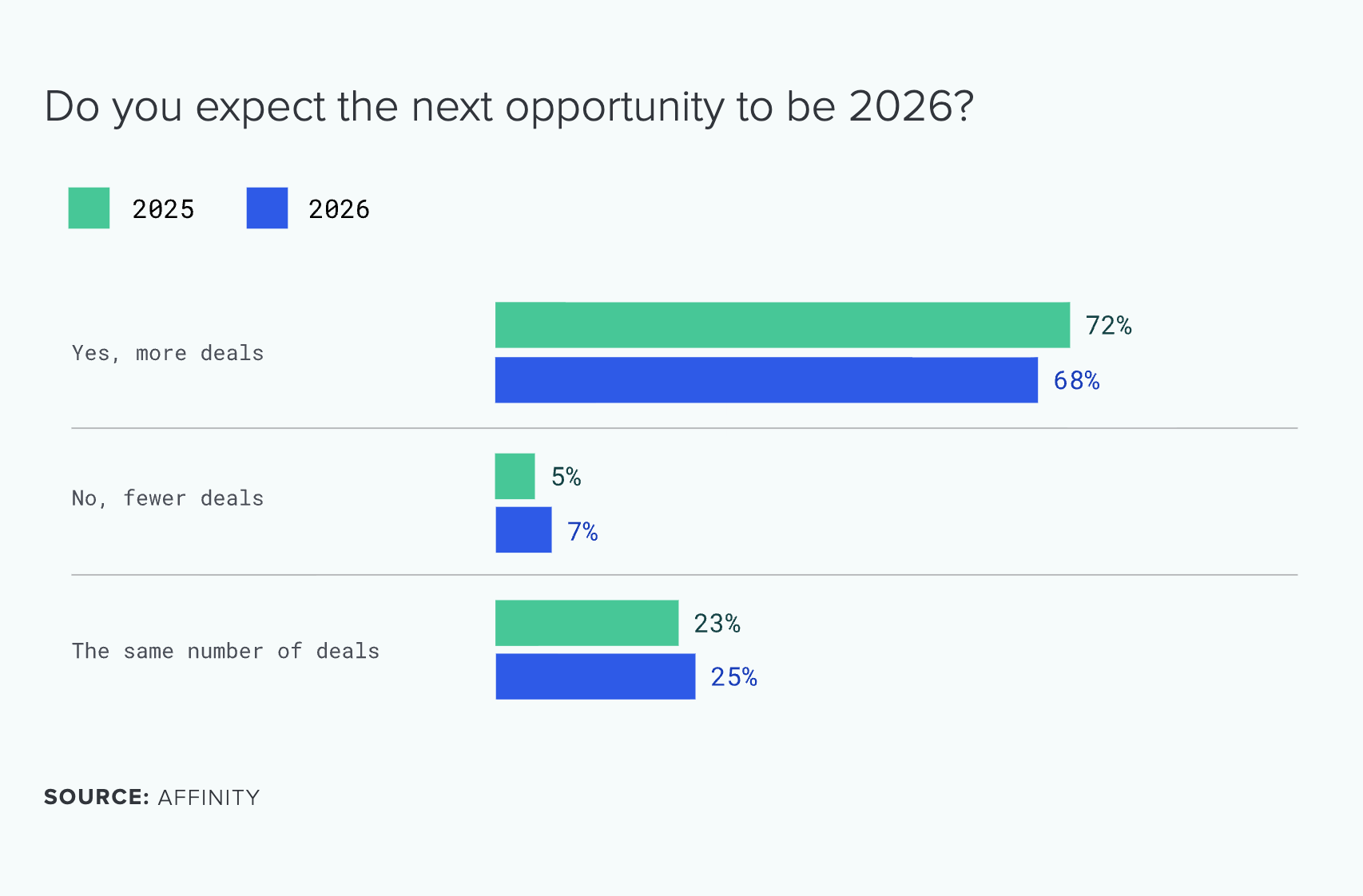

Deal volume expectations reflect measured optimism

Deal activity expectations remain strong heading into 2026, with 68% of investors anticipating increased volume—though slightly down from 72% the previous year.

This shift toward measured expectations doesn't indicate pessimism. Instead, it reflects a more sophisticated approach to deal-making—one that prioritizes quality and strategic fit over pure volume.

Economic outlook remains the dominant factor

Economic outlook dominates deal strategy for 2026, with 68% citing it as a major factor influencing volume—up 6 percentage points from last year. Meanwhile, competitive pressure is rising: 46% now view competition from other firms as significantly impacting their deal activity, compared to 42% previously.

This dual pressure—external market forces and intensifying competition—explains why deal sourcing efficiency remains paramount, even as the vast majority (68%) expect to increase deal volume.

“There is enough capital in private markets for technology assets to allow such assets to remain private if need be, which is an avenue most companies take. That means liquidity has to happen through secondaries as opposed to IPO / M&A.”

Andrea Roda

Principal, Balderton

Research intensity reveals hidden costs

New data from 2026 shows the scale of the research challenge facing firms. One third of dealmakers spend 21-40 hours per week researching deals, while 24% dedicate 41-60 hours weekly to this critical activity.

With this level of time investment, the imperative for efficient, data-driven sourcing becomes clear. Firms that can automate research tasks and surface relevant opportunities faster gain a substantial competitive advantage.

The efficiency imperative

The 2026 data reveals two seemingly contradictory trends: firms are consolidating to fewer data sources (with 47% now using just 1-3 sources), yet research time remains intensive: over half of investors spend 21+ hours per week on deal research, with nearly a quarter dedicating 41-60 hours weekly.

This creates a paradox. Investors need comprehensive information, but they're narrowing their tool sets.

The resolution lies in integration and intelligence. Firms that can aggregate diverse data signals into a single, intelligent platform gain dual advantages: they reduce complexity while increasing insight depth. This explains why deal sourcing efficiency remains a critical opportunity for data, even as the number of data sources contracts.

Top performers aren't choosing between breadth and depth—they're finding platforms that deliver both.

PREDICTION 03

The fundraising window will open, but proving value will define success

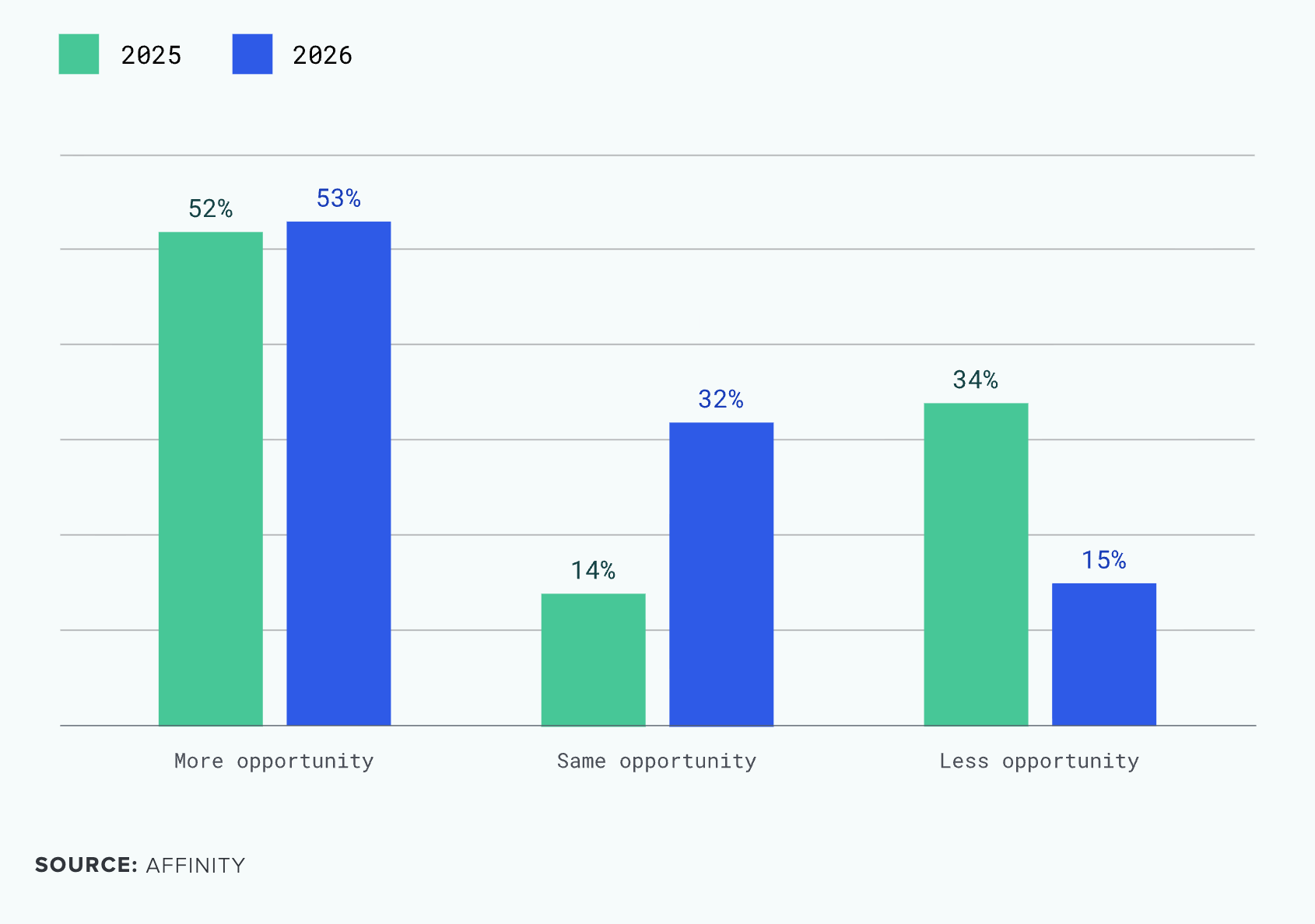

The most dramatic reversal in the 2026 survey results centers on fundraising sentiment. After years of challenging conditions, optimism has returned—but it comes with a critical caveat.

Fundraising optimism surges

The shift in fundraising outlook represents a complete transformation:

Do you see the opportunity to raise a fund as greater, less, or same as in 2025?

Fundraising sentiment has shifted dramatically. The share seeing 'less opportunity' collapsed from 34% to just 15%—a 19-point swing. Where did those pessimists go? Mostly to neutral ground: 32% now see 'same opportunity' (up from 14%), while 53% see improvement. The caution that dominated previous years has given way to stability and measured optimism.

"I think we’re going to see a real bifurcation in the market. The strongest companies will find healthy exit opportunities, whether through M&A or IPOs, at premium valuations. The rest will face a much tougher path, likely being forced to sell at a discount or remain private until they can strengthen their fundamentals enough to achieve a meaningful exit."

Nicole Bentz

Vice President, S3 Ventures

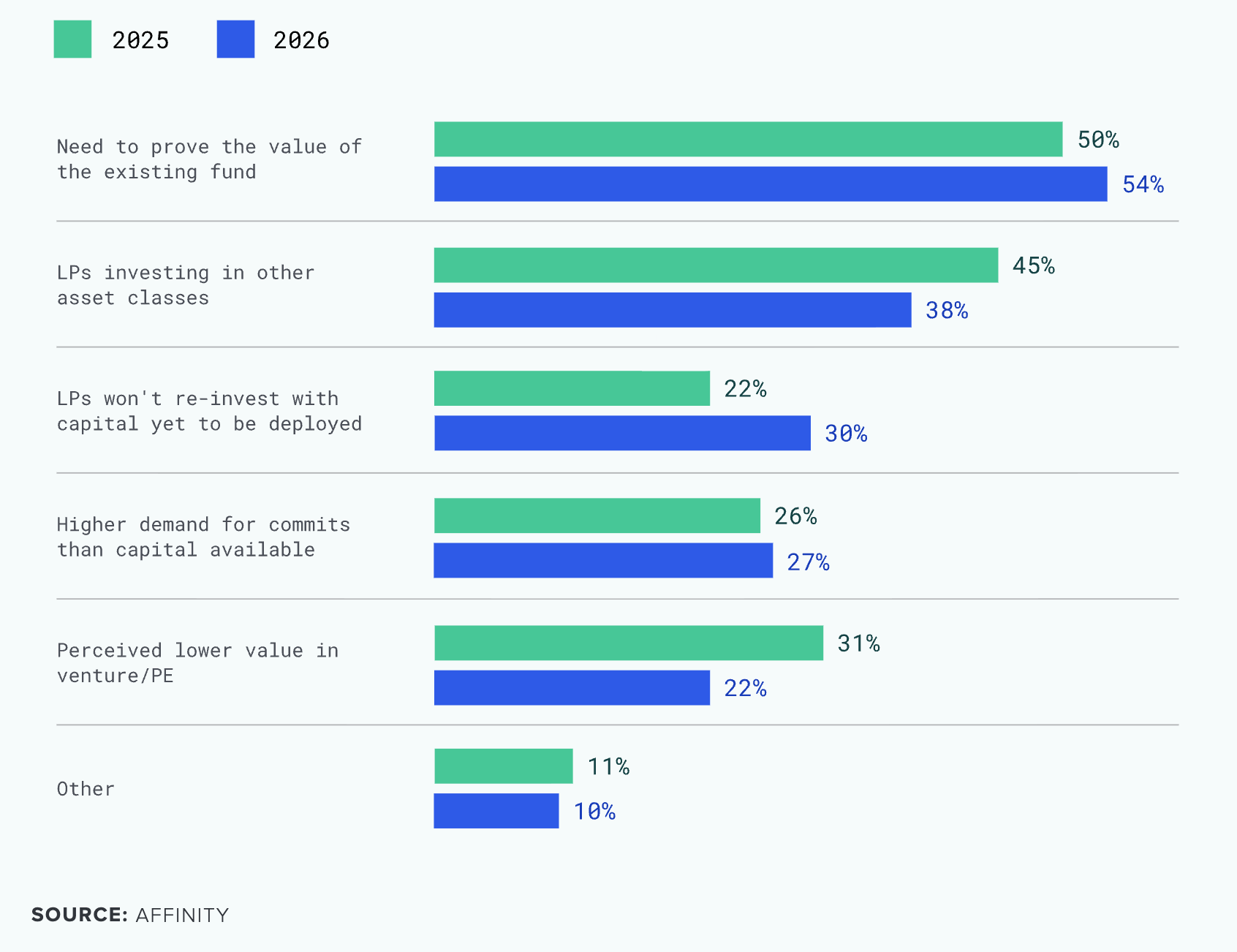

The bar for success keeps rising

Despite improved sentiment, the challenge of proving fund value has intensified:

What is most challenging in today's fundraising environment?

This creates an interesting tension: Opportunity is returning, but the bar for success is higher than ever. Simply having a track record isn't enough. Firms must demonstrate clear, compelling value creation to attract capital in an increasingly selective market.

“Fundraising is difficult to get the balance right, to knock on the right doors, and not waste peoples’ time. Try to research who you’re contacting, don’t just blast out messages. Just because AI can email everyone in the world doesn’t mean it should. Approach people that you’ve done some research on. Try to be more targeted so you can have more real conversations.”

Joe Schorge

Founder and Managing Partner, Isomer Capital

Source: Affinity

Quality over quantity becomes the mandate

Even as two-thirds of firms plan to increase deal volume, the slight pullback from 72% to 68% combined with sustained sourcing focus reveals a tension: firms want to do more deals, but they need to be more selective about which ones. Quality is becoming the differentiator.

Leading investors are asking better questions:

- How does each deal strengthen our portfolio thesis?

- What unique value do we bring to portfolio companies?

- How do we create differentiated outcomes that LPs can't access elsewhere?

The data-driven advantage

The convergence of fundraising opportunity and value demonstration pressure creates a unique moment for forward-thinking firms. LPs aren't just asking about returns; they're demanding evidence of how those returns were generated.

This shifts the conversation from storytelling to data storytelling. The firms that will win in this environment are those who can quantify their edge: sourcing efficiency metrics that prove superior deal flow, relationship intelligence that demonstrates proprietary access, and portfolio support analytics that show measurable value creation.

“In 2026, US unicorn exits are expected to rise modestly, led more by mergers and acquisitions than IPOs. IPOs will remain important but account for a small share of exits. Many unicorns may face valuation challenges or become stagnant. Secondary markets and strategic acquisitions offer more exit options. Valuations will be more realistic and capital efficiency will be emphasized. Overall, exit activity will be moderate with a cautious but optimistic outlook. The exit landscape is shifting from IPOs to diversified liquidity options. This reflects a new normal for unicorns and their investors.”

Javier Santiso

Principal, Mundi Ventures

The paradox of 2026 is that while opportunity is returning, the threshold for capturing it has never been higher. Beyond a baseline strong track record, success demands the ability to prove, with data, that your firm's approach is systematically superior.

In this environment, technology is the foundation for competitive differentiation.

CONCLUSION

What this means for 2026

Our three predictions reveal an interconnected story about how private capital is evolving:

AI becomes strategic, not just tactical

AI has crossed the threshold in 2026. The surge in AI for investment decisions more than doubling from 13% to 28% signals that technology has evolved into a strategic partner. Therefore, the competitive gap is widening: firms that have mastered AI-augmented decision-making are pulling ahead. Those still treating AI as a curiosity risk falling behind. The firms who have invested in deep AI integrations have set up the foundation for competitive advantage.

Efficiency through consolidation

The shift from 4-6 data sources to 1-3 core platforms isn't just about cost savings, it's about competitive advantage. As deal sourcing remains a top priority and research demands intensify, firms that successfully integrate comprehensive data into streamlined workflows will identify opportunities faster and make better-informed decisions. The winners won't be those with the most tools, but those with the most intelligent integration.

Data-driven differentiation defines fundraising success

Now that the fundraising opportunity has reopened, entry requirements have changed. LPs demand quantifiable evidence of value creation. That’s not just stories, but hard-hitting data. The quality of data depends on the sophistication of technology being used.

The challenge extends beyond proving value alone. LPs are simultaneously navigating competing priorities: 38% are allocating to other asset classes, 31% are hesitant to re-invest with capital still deployed, and 27% face higher demand for commits than available capital.

AI is lowering the cost to access specialized knowledge and increasing efficiency, it is also creating major changes in employment and fueling concerns of speculative bubbles in asset markets. As global competition intensifies and supply chains remain fragile, resilience and security have become central factors for investment decisions.

Firms that can demonstrate sourcing efficiency, relationship intelligence, and portfolio impact with hard metrics will capture the returning capital.

Make AI and data your competitive edge

Affinity is the leading relationship intelligence platform for dealmakers. With its AI-powered CRM, Affinity helps private capital firms, investment banks, and strategic acquirers find, manage, and close more deals by harnessing the power of their networks. Affinity is used by more than 3,000 customers across 80 countries to unlock relationship insights, drive efficiency, and win more opportunities.

About our data

This report is based on a survey conducted by Affinity from September 22, 2025 to October 31, 2025 of 275 private capital professionals across venture capital, private equity, growth equity, corporate venture capital, accelerators, & incubators.

The information in this report is provided for general informational purposes only. While efforts have been made to ensure its accuracy, no warranties or representations are made regarding the completeness or reliability of the content. Project Affinity, Inc. is not liable for any losses or damages arising from the use of this report. This report does not constitute professional advice. For specific concerns, consult a qualified expert.

.webp)

.webp)